Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  BNB

BNB  USDC

USDC  XRP

XRP  Solana

Solana  TRON

TRON  Figure Heloc

Figure Heloc  Hyperliquid

Hyperliquid  Dogecoin

Dogecoin  USDS

USDS  LEO Token

LEO Token  Wrapped stETH

Wrapped stETH  Zcash

Zcash  Stellar

Stellar  Wrapped Bitcoin

Wrapped Bitcoin  WhiteBIT Coin

WhiteBIT Coin  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Cardano

Cardano  Canton

Canton  Wrapped eETH

Wrapped eETH  USD1

USD1  sUSDS

sUSDS  Ethena USDe

Ethena USDe  Bitcoin Cash

Bitcoin Cash  Coinbase Wrapped BTC

Coinbase Wrapped BTC  Litecoin

Litecoin  Hedera

Hedera  Circle USYC

Circle USYC  WETH

WETH  Global Dollar

Global Dollar  Sui

Sui  Avalanche

Avalanche  USDT0

USDT0  LAB

LAB  Shiba Inu

Shiba Inu  NEAR Protocol

NEAR Protocol  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund  Ethena Staked USDe

Ethena Staked USDe  Ondo US Dollar Yield

Ondo US Dollar Yield  Bittensor

Bittensor  MemeCore

MemeCore  World Liberty Financial

World Liberty Financial  PAX Gold

PAX Gold  Aster

Aster  OKB

OKB  Ondo

Ondo  Ripple USD

Ripple USD  HTX DAO

HTX DAO  syrupUSDC

syrupUSDC  Polkadot

Polkadot  Falcon USD

Falcon USD  USDD

USDD  Worldcoin

Worldcoin  BFUSD

BFUSD  Aave

Aave  Pi Network

Pi Network  Sky

Sky  Jupiter Perpetuals Liquidity Provider Token

Jupiter Perpetuals Liquidity Provider Token  Pepe

Pepe  Quant

Quant  KuCoin

KuCoin  Spiko EU T-Bills Money Market Fund

Spiko EU T-Bills Money Market Fund  Jito Staked SOL

Jito Staked SOL  Audiera

Audiera  USDGO

USDGO  Janus Henderson Anemoy Treasury Fund

Janus Henderson Anemoy Treasury Fund  Binance-Peg WETH

Binance-Peg WETH  Rocket Pool ETH

Rocket Pool ETH  Stable

Stable  Render

Render  Binance Bridged USDC (BNB Smart Chain)

Binance Bridged USDC (BNB Smart Chain)  Cosmos Hub

Cosmos Hub  Jupiter

Jupiter  POL (ex-MATIC)

POL (ex-MATIC)  Function FBTC

Function FBTC  Algorand

Algorand  NEXO

NEXO  JUST

JUST  USDtb

USDtb  Ethena

Ethena  syrupUSDT

syrupUSDT  ADI

ADI  Gate

Gate  币安人生 (BinanceLife)

币安人生 (BinanceLife)  Binance Staked SOL

Binance Staked SOL  Janus Henderson Anemoy AAA CLO Fund

Janus Henderson Anemoy AAA CLO Fund  Beldex

Beldex  Spiko Amundi Overnight Swap Fund (EUR)

Spiko Amundi Overnight Swap Fund (EUR)  Venice Token

Venice Token  Pump.fun

Pump.fun  Filecoin

Filecoin  NEW X CEO IS BACK

NEW X CEO IS BACK  Polygon Bridged USDC (Polygon PoS)

Polygon Bridged USDC (Polygon PoS)  Solv Protocol BTC

Solv Protocol BTC  Flare

Flare  YLDS

YLDS  Usual USD

Usual USD  clBTC

clBTC  Lighter

Lighter  Midnight

Midnight  Aptos

Aptos  Arbitrum

Arbitrum  TrueUSD

TrueUSD  StakeWise Staked ETH

StakeWise Staked ETH  A7A5

A7A5  Kinetiq Staked HYPE

Kinetiq Staked HYPE  Aerodrome Finance

Aerodrome Finance  tBTC

tBTC  Injective

Injective  EURC

EURC  Ondo Short-Term U.S. Government Bond Fund

Ondo Short-Term U.S. Government Bond Fund  Artificial Superintelligence Alliance

Artificial Superintelligence Alliance  Hastra PRIME

Hastra PRIME  c8ntinuum

c8ntinuum  Official Trump

Official Trump  Mantle Staked Ether

Mantle Staked Ether  Pudgy Penguins

Pudgy Penguins  VeChain

VeChain  Polygon PoS Bridged DAI (Polygon POS)

Polygon PoS Bridged DAI (Polygon POS)  Jito

Jito  Bonk

Bonk  COCA

COCA  Virtuals Protocol

Virtuals Protocol  SPX6900

SPX6900  Liquid Staked ETH

Liquid Staked ETH  Celestia

Celestia  Arbitrum Bridged WBTC (Arbitrum One)

Arbitrum Bridged WBTC (Arbitrum One)  Terra Luna Classic

Terra Luna Classic  apxUSD

apxUSD  The9bit

The9bit  Sun Token

Sun Token  Wrapped Flare

Wrapped Flare  Pyth Network

Pyth Network  Curve DAO

Curve DAO  L2 Standard Bridged WETH (Base)

L2 Standard Bridged WETH (Base)  Ether.fi

Ether.fi  Steakhouse USDC Morpho Vault

Steakhouse USDC Morpho Vault  Kinesis Gold

Kinesis Gold  Grass

Grass  Bitcoin SV

Bitcoin SV  ETHGas

ETHGas  Binance-Peg XRP

Binance-Peg XRP  Ether.Fi Liquid ETH

Ether.Fi Liquid ETH  AINFT

AINFT  Noon

Noon  Olympus

Olympus  Plasma

Plasma  Jupiter Staked SOL

Jupiter Staked SOL  BUILDon

BUILDon  Savings USDD

Savings USDD  Monad

Monad  Legacy Frax Dollar

Legacy Frax Dollar  Marinade Staked SOL

Marinade Staked SOL  Conflux

Conflux

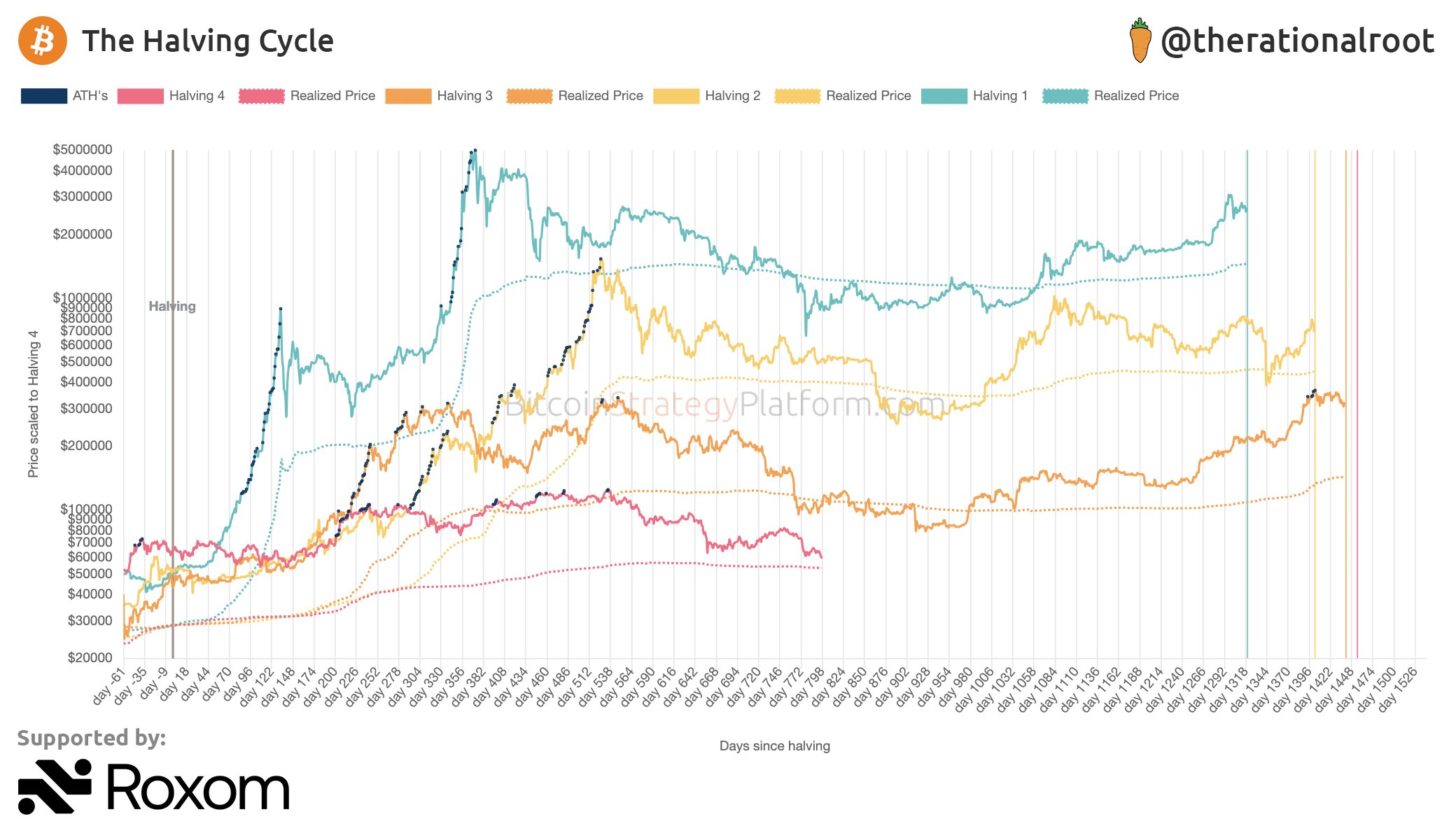

Most traders insist that this is the worst Bitcoin halving cycle in history, but data indicates the comparison may come from a skewed starting point.

These concerns have emerged due to Bitcoin’s ($BTC) performance since its fourth halving on April 19, 2024. The crypto asset now trades at $59,400, below the roughly $64,000 price it held on the day of the halving.

Bitcoin Halving-Day Buyers Still Underwater

This indicates that more than 800 days later, investors who bought Bitcoin on halving day are still sitting at a loss. This is the first time in Bitcoin’s history that halving-day buyers have remained underwater this far into a cycle. In every previous cycle, they were already in profit by this stage.

Bitcoin’s drop from its peak has also added to the concerns. Specifically, the crypto firstborn has fallen about 53% from its all-time high of around $126,000, reached on Oct. 6, 2025.

Now, while this decline is still smaller than the drops of more than 77% that followed the market peaks in 2018 and 2022, Bitcoin has not delivered the strong gains the market recorded in earlier cycles.

Skewed Starting Point

However, the halving date is a skewed starting point because this cycle began under conditions Bitcoin had never experienced before. Notably, $BTC had already reached a new all-time high of $73,800 on March 12, 2024, more than a month before the fourth halving.

This was a major change from previous cycles. In earlier halvings, Bitcoin had not yet moved above the previous bull market’s peak by the time the halving took place. As a result, on the halving day, the market still had room to climb before reaching new highs. This cycle followed a completely different path.

A major reason for the difference was the launch of U.S. spot Bitcoin ETFs in January 2024. These funds attracted massive institutional demand well before the halving reduced Bitcoin’s new supply. On the halving day, they had already attracted $12.3 billion in cumulative net inflows.

This early buying pushed Bitcoin’s price much higher before the halving even arrived, creating an unusually high starting point.

Realized Price Presents a Better Way to Compare Cycles

Many analysts consider realized price a better benchmark because it does not react as quickly to single events. Specifically, realized price measures the average cost of all coins in circulation based on the price at which each coin last moved on-chain.

Since realized price changes gradually as investors buy and sell Bitcoin, it is less affected by major events such as ETF approvals. This makes it a more stable way to compare different market cycles without the distortion created by Bitcoin’s unusually strong rally before the halving.

Bitcoin’s realized price currently stands at $53,197, while the spot price is around $59,400. That means the spot price trades at a premium of roughly 10% above the realized price, one of the smallest gaps seen during this cycle.

In past cycles, Bitcoin reached major market bottoms when the spot price moved this close to the realized price, including the lows recorded in 2015, late 2018 into 2019, and 2022.

Bitcoin Realized Price Still Shows This Has Been a Weak Cycle

Nonetheless, even after removing the effect of Bitcoin’s early rally, realized price does not make a bullish case for this cycle. Instead, it still points to weaker performance than previous halving periods.

During this cycle, the Bitcoin market price never moved far above realized price the way it did during the major bull market peaks of 2013, 2017, and 2021.

In those earlier cycles, heavy speculation pushed Bitcoin’s market value several times above the combined cost basis of all coins. Such a gap never developed this time, even when Bitcoin reached its record high in October 2025.

The smaller gap between spot price and realized price suggests this market has behaved differently from earlier ones. The current cycle has been shaped by steady institutional buying through spot Bitcoin ETFs instead of being driven mainly by retail speculation.

It is still too early to know whether this will lead to a smaller market bottom or simply a quieter bull market. However, while using realized price instead of the halving-day price removes the distortion caused by ETFs, it still indicates that the cycle has been worse than others at similar periods.